What Type of Investor Are You? A UK Guide to Risk Tolerance & Smarter Wealth Building

Transparency Disclosure: To keep our guides free for everyone, this post contains affiliate links and display advertisements. If you click an affiliate link and sign up, we may earn a commission at no extra cost to you. As an ex-banker with 25 years of experience, I only recommend tools that I believe provide genuine value to your financial health. Read our full Affiliate Disclosure here.

Understanding your risk attitude is like knowing your financial thermostat. It’s the level of uncertainty you can tolerate before you start losing sleep.

Some people are comfortable riding market ups and downs. Others prefer stability and certainty. Neither is right or wrong—but choosing the wrong strategy for your personality can quietly destroy your long-term wealth.

This guide will help you:

- Identify your risk profile

- Understand how it affects your decisions

- Build a portfolio you can actually stick with

Why Risk Tolerance Matters More Than Returns

Many people chase the highest returns. But in reality, returns don’t matter if you can’t stay invested.

During events like the COVID-19 market crash, millions of investors sold at the worst possible time—not because their strategy was wrong, but because it didn’t match their emotional tolerance for risk.

👉 Your real risk tolerance is revealed during market downturns—not bull markets.

The Three Investor Personalities

🛡️ 1. The Risk-Averse Investor (The Protector)

You prioritise capital preservation over high returns.

- You prefer stability and predictability

- Market volatility makes you uncomfortable

- You’d rather earn less than risk losing money

Motto: “A bird in the hand is worth two in the bush.”

⚖️ 2. The Risk-Neutral Investor (The Pragmatist)

You make decisions based on logic and expected outcomes.

- You accept that some risk is necessary

- You balance growth with stability

- You stay relatively calm during market swings

Motto: “Slow and steady wins the race.”

🚀 3. The Risk-Seeking Investor (The Pioneer)

You see risk as an opportunity.

- You’re comfortable with volatility

- You aim for higher, market-beating returns

- You’re willing to accept short-term losses

Motto: “Fortune favours the bold.”

⚠️ But here’s the reality:

Most risk seekers overestimate their ability to pick winners and underestimate how difficult it is to stay invested during sharp declines.

Quick Risk Assessment

Use this simple test to identify your profile.

📊 Risk Tolerance Calculator

Answer 5 quick questions to discover your investor profile.

“Knowing your risk profile is the first step. Building a plan you can stick with is what creates wealth.”

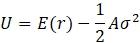

The Core Idea Behind Investing (Made Simple)

At its heart, investing is a trade-off between return and risk.

Where:

- U is the Utility (satisfaction).

- E(r) is the expected return.

- A is the coefficient of risk aversion.

is the variance (risk) of the portfolio.

is the variance (risk) of the portfolio.

In plain English:

- Higher returns increase satisfaction

- Higher risk reduces satisfaction

- The more risk-averse you are, the more you “penalise” risk

👉 The goal is not the highest return—it’s the best return you can emotionally handle.

Wealth Building Strategies by Risk Profile (UK Focus)

🛡️ Risk-Averse Strategy: Stability First

Asset Allocation (Guide):

- 70% Bonds / Fixed Income

- 20% Large-cap equities

- 10% Cash

Where to invest:

- Cash ISA

- Fixed-rate savings accounts

- Government bonds

- Dividend-paying UK stocks (e.g. FTSE 100 companies)

Key Tip:

Build an emergency fund of 6–12 months before investing.

⚖️ Risk-Neutral Strategy: Balanced Growth

Asset Allocation (Guide):

- 60% Equities

- 30% Bonds

- 10% Property / REITs

Where to invest:

- Stocks and Shares ISA

- Global index funds (e.g. MSCI World)

- UK equity exposure (FTSE 100)

Key Tip:

Rebalance your portfolio once a year—avoid reacting to short-term news.

🚀 Risk-Seeking Strategy: Growth Focused

Asset Allocation (Guide):

- 80% Growth equities

- 15% Alternatives (e.g. crypto, emerging markets)

- 5% Cash

Where to invest:

- Sector ETFs (technology, AI, biotech)

- Emerging markets

- Selected individual stocks

Key Tip:

Limit speculative assets to 10–20%—don’t let them dominate your portfolio.

The Most Important Rule: Time Horizon Beats Personality

This is where many investors go wrong.

Even if you’re a risk seeker, short-term goals should not be invested aggressively.

Example:

- Buying a house in 2–3 years → Low risk

- Retirement in 20+ years → Can take higher risk

👉 Your investment timeline should always override your risk attitude.

Final Thought: Can You Stick With Your Plan?

Most people believe they are confident investors—until markets fall.

The real question is not: “What type of investor am I?”

It’s: “Will I stick to this plan if my portfolio drops 30%?”

If the answer is no, your strategy needs adjusting.

Why Trust Bright Savings UK?

Bright Savings UK is run by a former banker with over 25 years of experience in the banking and financial services industry. Our goal is to help everyday people save smarter, with clear explanations and practical guidance.

Suggested Internal Links

- Risk vs. Opportunity: How to Manage Both at Every Stage of Life [Link]

- Mindset, Motivation & Discipline: The Real Foundations of Financial Freedom [Link]

- Be Water: A Timeless Philosophy for Building Wealth [Link]

How We Monetize This Site

To support the research and running of Bright Savings UK, we use two primary methods of monetization:

- Affiliate Links: Some links on this site are affiliate links. If you click and open an account, we may receive a commission. This does not change the price or terms you receive from the provider.

- Display Advertising: We host third-party advertisements through Google AdSense. We do not directly control the specific products shown in these ad units, and their presence does not constitute an endorsement by Bright Savings UK.

`

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Always review provider terms directly before applying.